What started as a new diabetes and weight loss treatment has become a massive expense for employer health plans—virtually overnight.

Last year, GLP-1 drugs like Wegovy and Ozempic accounted for roughly 9% of employers’ total annual medical claims, and demand isn’t slowing down anytime soon. Over 57 million adults under 65 could be eligible for a GLP-1 drug, but only 6% of US adults are taking one, making higher utilization (and higher costs for employers) almost inevitable.

Even enterprise employers are feeling the heat. In a recent McKinsey survey, “jumbo” employers said their biggest challenge in building a benefits package was managing employee interest in novel therapies like GLP-1 medications.

That puts brokers at the center of a tough balancing act: helping employers design plans that are both competitive and sustainable. In this guide, we explain:

- Why GLP-1s are so popular, and why that matters to your clients

- The real financial and plan design implications of covering GLP-1s

- How to use data and technology to manage client risk in a changing benefits landscape

The rise of GLP-1s: promise and pressure

What are GLP-1s?

Originally, GLP-1 receptor agonists were designed to treat type 2 diabetes. But researchers noticed that they also reduced appetite and slowed digestion—two key contributors to weight loss.

So, starting around 2014, certain GLP-1 drugs began getting FDA approval specifically for obesity and weight management.

Why have GLP-1s garnered so much attention?

Well, because they work: some people who’ve taken GLP-1s have lost 15% of their body weight. Many have also shown reduced risk of obesity-related complications, like heart and kidney problems.

These impressive results have both increased consumption and led to a broader public awareness of these drugs. Per Kaiser Family Foundation:

- 1 in 8 US Americans (12%) have taken a GLP-1.

- 32% say they’ve heard “a lot” about these drugs (up 13 percentage points since 2023).

Demand is meeting the bottom line

For employers, GLP-1s promise potential downstream cost savings. Improving the health of their employees now could mean lower long-term costs tied to chronic conditions later. Plus, adding GLP-1s to their health plans could improve employee satisfaction and retention.

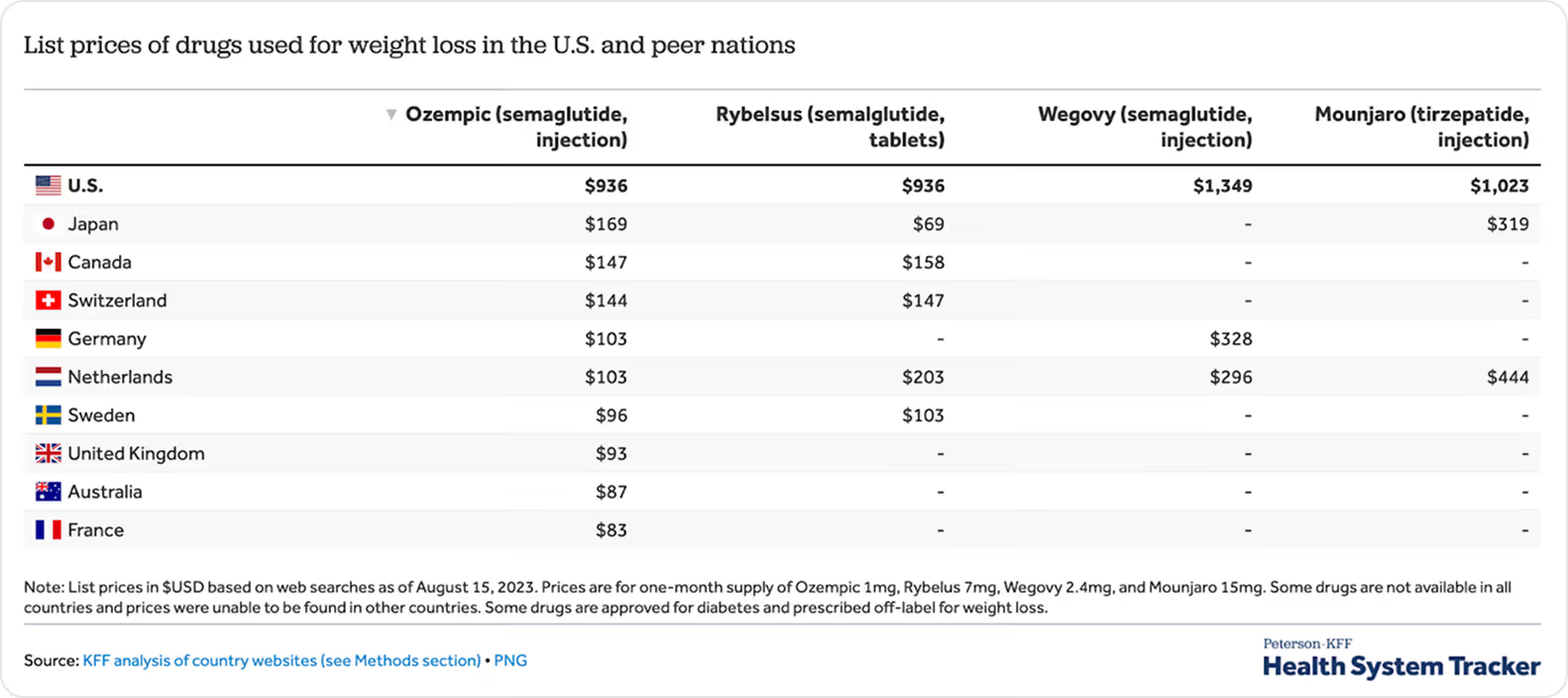

But the short-term math is harder to swallow. GLP-1s cost between $900 and $1,350 per month, over $10,000 per year per patient on the low end.

Employers are feeling the pressure, and that’s where brokers have an opportunity to step in by setting up plan structures that rein in costs but also appeal to great talent.

How GLP-1 adoption is impacting stop-loss and plan design

Recent data from Evernorth (Cigna’s health services division) shows that GLP-1s are fueling the fastest rise in traditional drug spending on record, even outpacing specialty drug growth for the first time. Here are three ways that surge is already reshaping employer plans and where brokers can make the biggest difference:

Stop-loss underwriting

Stop-loss carriers are growing more and more cautious about pharmacy exposure, and rightfully so. Not only are GLP-1s expensive, they’re designed for long-term use (likely over the entire course of someone’s employment).

Stealth Partner Group reports that the sharp increase in frequency of GLP-1 claims is drawing extra scrutiny, which could lead to increased premiums, added exclusions, and sublimits around obesity and weight loss prescriptions.

To avoid that, you’ll need to work with your clients to understand things like:

- How many members are currently using GLP-1 therapy

- What is the month-over-month trend in utilization (new starts, drop-offs, refill patterns)

- What is the average cost per member (or per user) on GLP-1 therapy

- What is the persistence or discontinuation rate within the plan population

And you’ll need to reassess those numbers every year to anticipate how stop-loss carriers might model risk for your clients, and how to negotiate during renewals.

Plan design and formularies

For employers that want to offer competitive health plans, it’s no longer a question of whether to cover GLP-1s, it’s how. Your role is to help them design coverage that satisfies employee demand and avoids uncontrolled costs.

These are a few levers you can pull:

- Utilization management. Among employers that cover GLP-1s, 78% use utilization management as a cost-control tool. 96% of those employers require prior authorization. 26% require reauthorization, 14% use a physician-led review, and others choose to require telehealth vendors.

- Eligibility requirements. Minimum BMI, diagnosis of obesity, or having nutrition or dietary criteria to limit coverage to particularly high-risk patients.

- Step therapy. Some plans require patients to try low cost or generic alternatives before getting GLP-1 therapy.

Employee expectations

Denying coverage can create friction, especially among leadership or high-earning employees who may push back directly. In fact, 67% of employees say they would be “likely” or “very likely” to stay at a job they didn’t like just to sustain coverage for weight loss medication.

It’s that important. And it’s why a third of employers now offer GLP-1s for diabetes and weight loss (up 2% from last year).

If your clients don’t cover GLP-1s, they’ll struggle to compete with employers offering broader coverage. Even for those who do, strict eligibility or utilization rules can cause resentment if employees feel left out or confused.

The best way to relieve that tension is transparency. Clear communication helps employees understand why guardrails exist and how they protect the plan’s sustainability while preserving access for those who need it most.

5 ways to position yourself as a strategic advisor on GLP-1s

Your clients want to make smart, sustainable decisions about GLP-1 coverage. Brokers who can explain the why behind GLP-1 decisions and build proactive cost-control strategies will quickly become indispensable partners—not just intermediaries.

Here’s how to stand out:

1. Educate clients on the full cost curve

Most employers view GLP-1s as an immediate hit to their pharmacy budget. In some ways, that’s true. Like we mentioned, these drugs can cost up to $1,350 per patient per month.

At the same time, GLP-1s yield meaningful indirect health savings, such as lower rates of diabetes and other reduced comorbidities from obesity, which can decrease future medical claims. Novo Nordisk, the manufacturer of Wegovy, showed that semaglutide reduced kidney disease progression, major cardiovascular side effects, and death by 24% (as compared to a placebo).

But those gains only materialize if patients stay on the drugs indefinitely, which means costs compound every year the plan covers them. Extended use can also distort risk modeling for stop-loss carriers, potentially leading to premium hikes and new coverage exclusions.

Your clients need visibility into how these gains and losses balance out. Partner with finance leaders to model multi-year scenarios and see how utilization and adherence might impact health outcomes and total cost of care. Then, recommend appropriate coverage criteria.

2. Explore outcomes-based programs

One way to make GLP-1 coverage more sustainable is to tie cost to performance. Outcomes-based programs, also called results-based pricing, link payment to measurable health improvements, such as sustained weight loss or improved cholesterol and blood pressure readings.

Some PBMs (pharmacy benefit managers) and specialty vendors are already experimenting with these kinds of contracts. Employers only pay the full cost of treatment if the therapy delivers the intended results. If not, the manufacturer or PBM shares part of the cost.

For you, this means:

- Researching PBMs or vendors offering outcomes-based GLP-1 programs.

- Assisting clients in evaluating which metrics (weight reduction, metabolic improvements, or adherence) best suit their workforce.

- Recommending other up-and-coming programs that align incentives between employers, members, and manufacturers that your clients can take advantage of.

3. Leverage tiered formularies

Managing who qualifies for GLP-1s, when, and at what cost can get complex fast. Tiered formularies give clients flexibility to offer care without eliminating coverage entirely.

As a reminder, formularies determine how drugs are categorized (typically by cost, clinical effectiveness, or necessity) and how much the plan pays for each. Placing GLP-1s in a higher formulary tier or requiring additional steps before approval keeps access aligned with medical need rather than general demand.

You can help your clients:

- Develop utilization controls

- Translate utilization controls into clear, fair policy language.

- Collaborate with PBMs to track adherence and prior-authorization data over time.

- Regularly review formulary performance and make adjustments as demand and clinical guidelines evolve.

4. Review stop-loss renewals early

As we pointed out earlier, stop-loss carriers are watching GLP-1 utilization closely. You can help clients avoid surprises by gathering utilization and cost data ahead of renewal season. Presenting this data early gives you a lot more leverage in renewal discussions and helps you flag exposure before underwriters price it in.

Early analysis also gives clients time to implement cost-control measures before renewal, strengthening their financial position (and positioning you as a trusted advisor).

5. Integrate with wellness programs

GLP-1s work best when they’re part of a broader metabolic health strategy. Without continued lifestyle support, results fade quickly. People who had been taking Wegovy along with a lifestyle intervention regained two-thirds of the weight they had lost a year after coming off the drug.

Encourage employers to connect GLP-1 coverage to nutrition coaching, fitness benefits, and behavioral health resources. These investments help employees sustain their progress, improve their mental health, and stay engaged at work. They also signal that the company cares about employee wellbeing, which can strengthen retention and productivity—all while keeping healthcare costs in check.

Solidify your clients’ GLP-1 strategy now

GLP-1s may be today’s hot topic, but they won’t be the last high-cost therapy to reshape employer health plans. As new treatments and programs gain traction, your clients will ask the same hard questions about cost, access, and outcomes.

ThreeFlow gives brokers the time and visibility to lead those conversations. By automating plan marketing and centralizing data, you can spend less time on logistics and more time advising clients on emerging cost drivers, whether they’re drugs, vendors, or compliance rules.

How you respond to GLP-1s now can (1) serve as a framework for the next wave of cost-driving drugs and (2) highlight your value as a strategic partner—someone clients will immediately turn to for guidance when they need it.

Schedule a demo to see how ThreeFlow helps brokers anticipate new trends before they hit client budgets.

Share Article

Subscribe to our blog

JUMP TO SECTION

How will this change the way we work?

Does it fit how we work today?

How does this platform protect my clients, my data, and my reputation?

Who is using your platform and how?

Will this software grow with us?

What truly sets this platform apart?

How does the pricing model align with our revenue model?

What happens after go-live?

How does the platform use AI right now?

How will this change the way we work?

Does it fit how we work today?

How does this platform protect my clients, my data, and my reputation?

Who is using your platform and how?

Will this software grow with us?

What truly sets this platform apart?

How does the pricing model align with our revenue model?

What happens after go-live?

How does the platform use AI right now?

%20(1).avif)